- Phone: +27 83 776 6416

- Email: hello@howl.co.za

South Africa’s Crypto Boom and Busts

South Africa’s crypto boom created genuine innovation, genuine arbitrage opportunities and a hard-earned lesson in spotting old-fashioned fraud behind new technology.

Disclosure: This article is for general information only. It is not financial, tax or legal advice. Howl has received no referral fees, commissions, advertising payments or other kickbacks from any business mentioned here.

South Africa’s crypto story is not simply a list of scams.

The country built one of Africa’s more active crypto markets, developed a real crypto-arbitrage industry, and produced fintech teams with hard-won experience in compliance, exchange integration and cross-border money movement. But the boom also attracted operators selling impossible certainty: fixed returns, secret bots, referral rewards and dashboards that looked more convincing than the underlying businesses.

The encouraging part is that many of the worst schemes were exposed. Courts, regulators and law-enforcement agencies became involved. At the same time, legitimate providers were forced to become more transparent and more compliance-focused.

Five crypto schemes South Africans should remember

-

Mirror Trading International (MTI): MTI claimed to use an automated Bitcoin trading bot and rewarded members for recruiting others. The Western Cape High Court later found the business illegal, unlawful and fraudulent. Founder Johann Steynberg was arrested in Brazil, while the liquidation process expanded across several jurisdictions.1

-

Crypto Mzansi: Crypto Mzansi used social-media marketing, high-return promises and referral incentives. In 2025, founder Mfundo Manci pleaded guilty to fraud-related offences, received 10 years’ direct imprisonment, and had more than R4.5 million forfeited.2

-

CBI X and CBI Exchange Namibia: CBI used crypto branding, network-driven recruitment and claimed weekly returns of 1% to 4%. After the South African operation drew attention, a similar model emerged in Namibia. Coenraad “Coenie” Botha and Charlotte Murove face criminal charges there, including fraud, money laundering and unauthorised banking activity. They have pleaded not guilty, so the matter remains unresolved.3

-

Africrypt: Africrypt collapsed after claiming a hack had compromised client accounts. The amount of Bitcoin involved remains disputed, and the wider case has not produced a final criminal conviction. It remains a useful warning about custody, unverified trading claims and the difficulty of recovering assets once money and people move across borders.4

-

GS Partners: GS Partners mixed crypto, metaverse language and affiliate marketing. The FSCA warned that it was not licensed to provide financial products or services in South Africa and raised concerns about unrealistic returns. A local promoter was later arrested on a fraud allegation; that arrest is not a conviction.5

The punchline: there is no honest single figure for “all crypto losses” because several cases remain disputed or unresolved. MTI alone recorded roughly 35,500 Bitcoin flowing into its wallets, valued by SARS at about R6.85 billion at the time. Liquidators recovered and sold 1,281 Bitcoin for roughly R1.05 billion. Recovery can happen, but it is usually partial, slow and far less exciting than the original promises.6

Arbitrage was different

Crypto arbitrage should not be confused with a Ponzi scheme.

Arbitrage is a transaction strategy: buy a crypto asset in one market, sell it in another market where the price is higher, and retain the difference after foreign-exchange costs, trading fees, tax and service fees. It does not depend on Bitcoin rising in price. It depends on a temporary price gap between markets.

For years, South African crypto markets traded at a premium to offshore markets. That created a genuine opportunity for firms that could execute trades efficiently, handle foreign-exchange rules and settle transactions reliably.

The historical data at ZArbitrage tells the story well: premiums rose sharply during the boom years and then narrowed as the market became more competitive, more regulated and more efficient.7

The difficult part was never only Bitcoin

Arbitrage requires more than buying and selling crypto. It requires converting rands into foreign currency, remitting funds offshore, documenting the transaction and complying with exchange-control and anti-money-laundering rules.

That was one of the sector’s early bottlenecks. FNB announced in 2019 that it would withdraw services from cryptocurrency platforms from March 2020, and Standard Bank later closed accounts held by certain automated crypto-arbitrage businesses. Those were historical de-risking decisions taken while the sector’s compliance environment was still developing; they should not be read as statements about either bank’s current policy.8

This is why specialist forex infrastructure matters. In the Fynbos Arbitrage process, Kuda FX handles the foreign-exchange and offshore-remittance leg. It is not the crypto trade itself. It is part of the financial plumbing that allows a compliant arbitrage cycle to happen.9

A credible provider should be able to explain that plumbing clearly: who converts the currency, which legal entities handle the funds, where the crypto is bought and sold, what the fees are, and what happens when banking or settlement delays occur.

What happened to the early arbitrage firms?

The market matured.

Koinexpert is a useful positive example. Over roughly 2.5 years, it processed more than R3 billion in trading volume while solving real problems around exchange integration, compliance and high-volume fintech operations. As margins narrowed and regulatory overhead increased, Currency Hub took over arbitrage trading for Koinexpert clients in 2023.10

The experience did not disappear. The former Koinexpert team went on to build Teruza, applying those lessons to professional fintech, automation and software systems. That is one of the better outcomes of the boom years: expertise gained in a difficult crypto market can become durable capability in mainstream fintech.

Other firms made similar commercial decisions. OVEX closed its arbitrage service in 2022 while continuing to operate other crypto-business lines. Shiftly closed its arbitrage service on 31 October 2025. Neither closure is evidence of fraud. It reflects the reality that an activity becomes harder to operate when margins shrink and compliance costs rise.11

Providers still visible in the market

The market is smaller than it was during the boom, but several providers still publicly offer crypto-arbitrage services, including:

These are not recommendations and do not guarantee profit or capital protection. Before using any provider, verify the legal entity, current FSCA status, foreign-exchange arrangements, costs, tax implications and withdrawal process. A licence is a starting point for due diligence, not a substitute for it.12

A practical 12% rule

There is no law saying that a return above 12% per year is automatically a scam. But it is a useful personal screening rule.

Any provider promising a guaranteed return above 12% per year deserves serious scrutiny. Ask where the return comes from, who carries the loss if the trade fails, whether the capital is truly protected, and why the offer beats ordinary regulated savings products by such a large margin.

For comparison, as at June 2026, RateCompare lists GoTyme’s GoalSave Bonus Rate with 10 days’ notice as its highest-paying savings-account option, at up to 10% per year. GoTyme’s own terms make clear that the rate depends on meeting its conditions, including the notice requirement. This is not a crypto return. It is a bank savings rate with defined terms.13

Fedgroup provides another useful benchmark: its Secured Investment is a five-year fixed-term product. The exact rate is set when the investment is made, and the five-year commitment is part of the trade-off. Legitimate returns are usually tied to time, liquidity restrictions, product risk and transparent terms.

That is very different from a promise of 4% every week from an unnamed bot, a secret strategy or a referral network.

Legitimate crypto returns can be boring

Not every crypto-related return is a scam.

Luno, for example, offers staking on supported crypto assets for South African customers. The annual reward percentage is displayed before staking and varies by asset and network conditions. A low-single-digit annual reward, such as around 4% on a supported asset, is plausible. It is also not guaranteed in rand terms: the underlying crypto asset can still fall sharply in price.14

That is the key distinction. A legitimate product explains its risks. It does not hide them behind mystery, urgency or referral commissions.

The quiet winners: HODLers

Looking back, some of Bitcoin’s biggest winners have been long-term holders: people who bought, held through volatility, avoided leverage and did not hand their coins to opaque yield schemes.

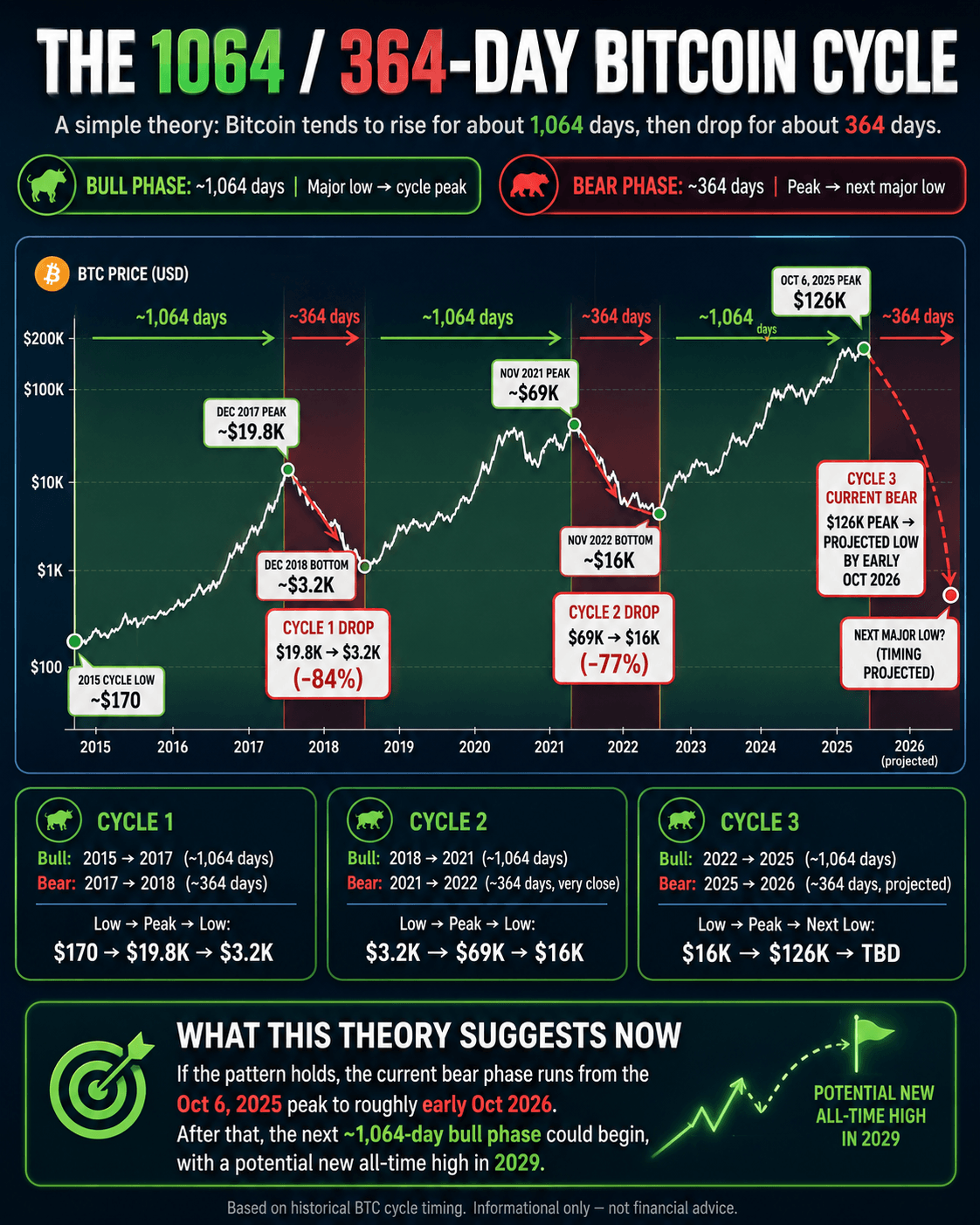

Bitcoin’s historical cycles are striking, but they are not a reliable timetable for future returns. The graph may reveal an interesting rhythm: Bitcoin has often moved in broad multi-year cycles, with long recoveries and advances from major lows followed by shorter, painful declines. But the exact timing is not fixed, the sample size is small, and history is not a forecast.

That uncertainty is part of Bitcoin’s appeal. More than 17 years after its launch, the identity of Satoshi Nakamoto remains unconfirmed. Bitcoin is now a global asset, but some of the mystery that made people pay attention in the first place remains.

The positive takeaway

South Africa’s crypto market is more mature than it was during the boom.

Major schemes have been exposed. Courts have acted. Regulators have become more active. Arbitrage providers have had to improve their controls. And the skills built during the early days have carried over into stronger fintech businesses.

Crypto still carries risk. Arbitrage still carries risk. Savings products, staking and Bitcoin itself all carry risk.

But a legitimate provider can explain where your money goes, how returns are generated, what it costs, what can go wrong and how you get your money back.

A scam needs mystery, urgency and new investors.

Sources

- Western Cape High Court judgment on MTI

- National Prosecuting Authority: Crypto Mzansi conviction and forfeiture

- Bank of Namibia: CBI Exchange Namibia investigation; The Namibian: Botha and Murove’s not-guilty pleas

- Reuters: Africrypt’s reported collapse

- FSCA warning on GS Partners

- Moneyweb: MTI recovery figures

- ZArbitrage: historical South African arbitrage spread

- Luno statement on FNB’s 2020 service withdrawal; MyBroadband: Standard Bank account terminations in 2021

- Fynbos Arbitrage: Kuda FX remittance role

- Moneyweb: Currency Hub taking over Koinexpert clients; Teruza: Koinexpert platform experience

- Moneyweb: OVEX exit from arbitrage; Shiftly: arbitrage-service closure

- Fynbos Finance; Currency Hub; Future Forex

- RateCompare savings-account comparison; GoTyme GoalSave terms; Fedgroup Secured Investment

- Luno: staking rewards; Luno: staking availability in South Africa